FTB 15-Day Rule, Prop 19 to Save $800 min. tax

Get a jump start on forming new entities and/or transferring properties before year-end to avoid the minimum $800 Franchise Tax Board for the tax year. This coupled with Prop 19’s adoption effective February 15, 2021, makes this the perfect time of year to form and fund your new LLCs or other business entities.

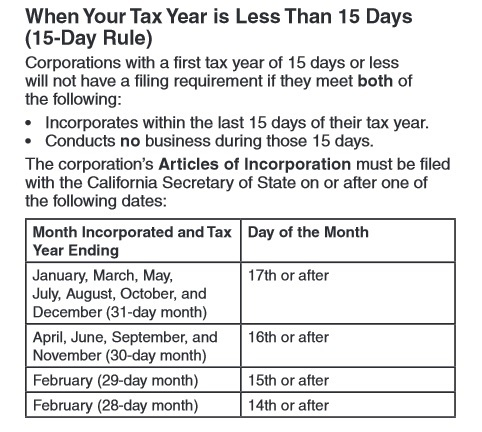

Tax Year of 15-Day or Less

A corporation that files within the last 15 days of the year, and does not engage in any business during those 15 days, would not need to pay the $800 minimum tax the following year.

For example, Acme, Inc. files its Articles of Incorporation with the California Secretary of State on December 18, 2020. The corporation does not engage in any business activity between December 17 and December 31, 2020.

Looking to get a head start with your California corporation or LLC and avoid potential filing backlogs right after the New Year? Consider incorporating or forming an LLC between December 17 and December 31.

California’s 15-day rule allows you to incorporate or form an LLC during the last 15 days of the year and avoid filing tax returns for 2020.

California Corporations

Pursuant to California Franchise Tax Board Publication 1060, corporations with a tax year of 15 days or less will not need file a tax return as long they do not conduct any business during those days:

CA Prop 19 New Tax Changes

With the passage of CA Prop 19 this year, certain and significant changes to estate planning considerations and strategies came along with it. Most notably, the ability to transfer intergenerational property at low assessed values (i.e., the assessed value at the original time of purchase) to avoid property tax reassessments to current values has been eliminated, except for very narrow exceptions. These changes are set to take effect on February 15, 2021.

By forming a corporate entity very specifically, families may be able to avoid transfer limitations and tax reassessments to preserve the ability for future generations to continue holding these assets, particularly for income-generating properties.

Testimonials

John Schroeder was brought on to work on my case with Samantha and they updated/collaborated with Noelle. Noelle, Samantha and John are all patient, direct and very personable. Their knowledge and professionalism are exceptional. NM Law was successful in achieving a Settlement Agreement under difficult circumstances amongst people with little trust in one another. Thankfully we did not have to bear the cost of going to trial, however, I have complete confidence that NM Law would have prevailed if we had.

I highly recommend NM Law. I look forward to working with them again, but this time to plan my estate.

I want to thank you and your staff for the courtesy extended to us during our family's pending emergency deadline.

Mr. O'Grady spoke to my brother and gave us his best recommendation regarding my father's estate.

It is really hard to speak, and even harder to "plan" generational wealth with a parent in terms of assets, intentions, and mortality, but it is a necessary conversation to have, if only to lessen the unfairness of life that eventually catches up to all of us.

Our family tried to bring justice to my father's death within this probate process and found no justice, this system must be changed, so that a fairness is inherit within this system and not just a scam—lots of hard lessons to be learned from a broken probate process.

In either case, thank you again for giving our family the attention and direction we sought. The adage is true, not all lawyers are the same. Looking forward to working with your office in the near future, as we don't want to repeat this experience with our Mom.

Gracias,

Abraham

We highly recommend NM Law for your estate planning needs.

I highly recommend NM Law.

Charities We Support

We dedicate pro bono time, volunteer services, and a percentage of our gross revenue to these organizations. In 2023, we sponsored a refugee family of five to come to the United States and start a new life.

Each year our law firm decides as a group which charities to assist with our time, money, and expertise. Please feel free to click on any of the charities below and make a donation of your own.